What Does Travel Insurance Cover?

Most travellers buy travel insurance just before a trip without really understanding what it covers. It often gets added during flight or hotel booking and many people purchase the cheapest policy available without checking whether it actually protects them. That can become a problem when something unexpected happens.

A medical emergency in Europe can cost Rs 5 lakh to Rs 20 lakh without coverage. A cancelled flight on a non-refundable ticket is gone money. A lost bag with your passport in it is a consular nightmare. Travel insurance exists precisely for these situations and in 2026 you can get a meaningful plan for as little as Rs 20 to Rs 30 per day.

Quick Answer

Here is what a standard travel insurance policy may cover:

Emergency medical treatment and hospitalisation

Emergency medical evacuation

Trip cancellation or interruption

Flight delays

Lost or delayed baggage

Passport loss

Personal accident

Personal liability

The exact coverage depends on the insurer and the plan you choose. Every policy also has its own limits, exclusions, deductibles and claim conditions so it is important to read the policy wording before purchasing.

What Is Travel Insurance?

Think of travel insurance as a financial safety net for your journey.

If something unexpected happens while you are travelling whether it is a medical emergency, delayed baggage, a cancelled trip or a lost passport your policy may help cover the financial loss provided the incident is covered under your plan.

You can buy travel insurance for a single trip, multiple trips throughout the year or even for specific travel needs such as family holidays, student travel or senior citizen travel.

The purpose is not to eliminate every travel problem. It is to reduce the financial impact when something covered goes wrong.

Key Benefits Covered by Travel Insurance

Most travel insurance policies cover the same broad areas. The biggest difference between plans is usually the coverage limit, exclusions and claim conditions.

Medical Expenses

Medical expenses are the most important cover and the main reason to buy travel insurance at all. A hospitalisation abroad without insurance can financially devastate a family. Medical cover pays for treatment costs due to an accident or sudden illness during the trip including hospitalisation, doctor fees and in serious cases emergency medical evacuation back to India.

Loss of Checked-In Baggage

Checked baggage doesn't always arrive when you do.

If your baggage is delayed, many policies reimburse the cost of essential items until it arrives. If the airline permanently loses your checked baggage, your policy may compensate you for the loss, subject to the coverage limit and policy conditions.

Note that this is different from baggage delay as many plans cover both but at different limits.

Loss of Passport

Loss of passport covers the emergency expenses involved in getting a replacement passport or emergency travel document when your passport is lost or stolen abroad. Consular fees, police report charges and related costs are typically covered.

Trip Cancellation

Trip cancellation covers non-refundable travel costs including flights, hotels and tour packages when you have to cancel the trip due to a covered reason. Covered reasons usually include sudden illness or injury, death of a family member or a natural disaster at the destination.

Voluntary cancellations or changes in travel plans are generally not covered.

Flight Delays

If your flight is delayed beyond the waiting period mentioned in your policy, you may receive compensation for meals, accommodation or other essential expenses incurred because of the delay. Some plans may also offer protection for missed connecting flights.

Personal Accident

A personal accident provides a lump sum or compensation in the event of accidental death or permanent disability during the trip. This is separate from medical cover and is paid regardless of treatment costs incurred.

Personal Liability

Personal liability covers you if you accidentally injure someone or damage their property during your trip. The policy pays up to the liability limit stated in the plan.

What Does "Covered" Actually Mean?

This is the part most travellers skip and it is often why claims fall short of expectations.

A listed benefit may still come with:

Sum insured: the maximum the insurer will pay in total

Sub-limit: a smaller cap that applies within the overall cover

Deductible or excess: the amount you pay before the insurer steps in

Time threshold: flight or baggage delay cover may only begin after a minimum number of hours

Per-item limit: baggage compensation may be capped for each individual item

Covered reasons: Some benefits, such as trip cancellation apply only for reasons specifically mentioned in the policy.

Knowing these before you buy is what separates a policy that helps when something goes wrong from one that disappoints.

What Travel Insurance May Not Cover

Travel insurance protects you against unexpected events, but it doesn't cover everything.

Common exclusions include:

Pre-existing medical conditions unless specifically covered

Adventure sports not included in the policy

Alcohol or drug-related incidents

Travelling against medical advice

Unattended baggage

Voluntary trip cancellations

Claims without supporting documents

Always declare known medical conditions accurately and check the policy wording before buying. Failing to disclose a known condition can lead to a claim being reduced or rejected particularly when the treatment is connected to that condition.

When Do I Need Travel Insurance?

Not every trip needs a policy but not every trip is safe to leave uninsured. Here is a quick gut-check:

Trip Type | Should You Consider Travel Insurance? | Why |

Schengen visa application | Required | Travel medical insurance equivalent to approximately ₹32.6 lakh must cover emergency care, hospitalisation and repatriation and remain valid across the Schengen area for the full stay |

Expensive international trip | Yes | Medical, cancellation and baggage risks can be costly |

Domestic short trip | Optional | Useful mainly for delays, baggage issues or prepaid bookings |

Trip with adventure activities | Yes, but check policy | Standard plans may exclude risky activities |

Trip with travel insurance benefits on a credit card | Check first | Cover may require booking with that card, activating the benefit or meeting age and trip-duration conditions |

If your trip falls into more than one row, compare a policy properly before deciding.

How Much Does Travel Insurance Cost?

Travel insurance is cheaper than most people expect. The cost depends on four things: where you are going, your age, the sum insured and the trip duration.

For example a week-long trip to Southeast Asia may cost less to insure than a month-long trip to the United States because healthcare costs and risk levels vary by destination.

On SaveSage, eligible travel insurance plans start from around ₹20 per day depending on your destination, age, travel dates and the coverage you choose.

International Travel Insurance on SaveSage

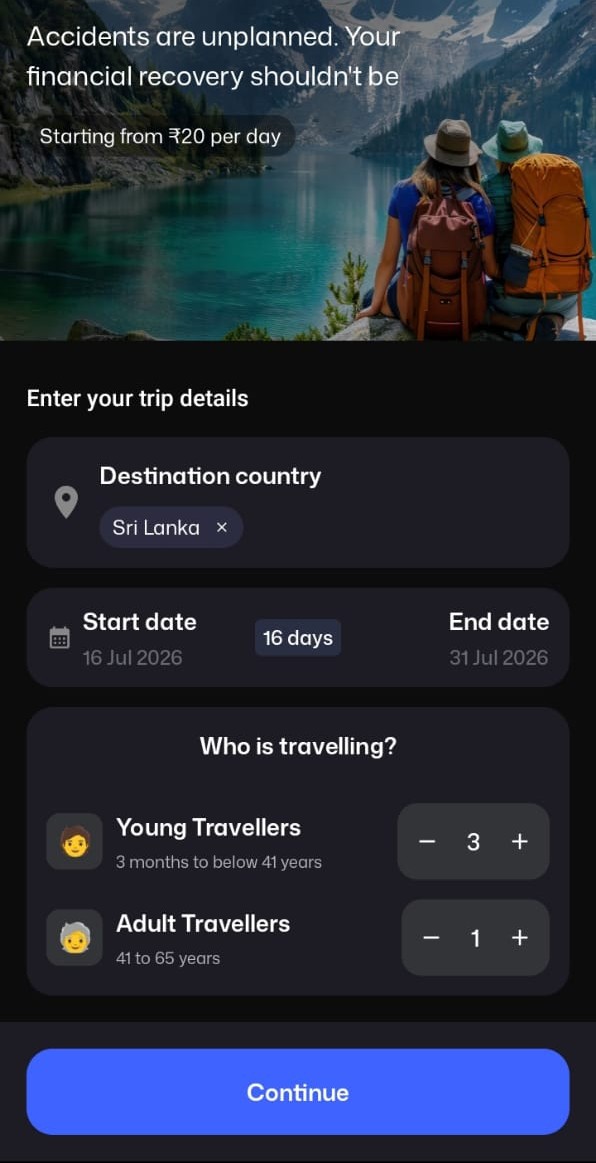

Finding the right travel insurance does not have to be complicated.

With SaveSage, you can compare International Travel Insurance plans from trusted insurance partners based on your destination, travel dates and the number of travellers.

Buying a policy takes just a few minutes.

Open the SaveSage app

Go to the Travel Insurance section

Enter your destination and travel dates

Add the number of travellers

Compare available plans

Choose the policy that best suits your trip and complete your purchase

Eligible plans start from around just ₹20 per day making travel insurance one of the simplest ways to protect your trip before you fly.

How to Choose the Right Travel Insurance Plan

Price should not be the only factor when comparing travel insurance. Before buying a policy check:

Whether it covers your destination and travel dates

The medical coverage amount and whether it meets visa requirements

The claim process and emergency assistance available

Deductibles and sub-limits

Common exclusions

The insurer's claim support and reputation

A policy with a slightly higher premium may provide significantly better protection when you actually need to make a claim.

SaveSage now offers travel insurance on its platform making it one more thing you can sort alongside your credit card rewards, points tracking and financial planning all in one place. If you are planning an international trip and want to understand which credit card benefits apply, how to track your reward points and how to protect the trip itself, SaveSage covers all three.

FAQs

What does travel insurance cover?

Travel insurance commonly covers emergency medical treatment, hospitalisation, emergency evacuation, trip cancellation or interruption, flight delays, baggage delay or loss, passport loss, personal accidents and personal liability. The exact benefits, limits and exclusions depend on the policy and insurer.

Does travel insurance cover pre-existing diseases?

Many standard policies exclude treatment linked to pre-existing conditions. Some plans may offer limited emergency cover or an optional extension but terms vary. Always declare known conditions accurately and check the policy wording before buying.

How much medical cover should I choose for an international trip?

The right amount depends on your destination, visa requirements and local healthcare costs. Choose enough cover for emergency treatment, hospitalisation and evacuation, and confirm that it meets any applicable visa requirements.

Is travel insurance mandatory for a Schengen visa?

Yes. Qualifying travel medical insurance equivalent to approximately ₹32.6 lakh is required for emergency care, hospitalisation and repatriation. The policy must remain valid across the Schengen area for the full duration of your stay. The exact rupee equivalent may change with exchange rates.

Does travel insurance cover flight cancellation or delay?

It may but only under conditions listed in the policy. Flight delay benefits usually apply after a minimum delay period while trip cancellation generally covers only specified reasons. Airline refunds or compensation may also be considered before the insurer calculates the payable amount.